Prior to the enactment of the SECURE (Setting Every Community Up for Retirement Enhancement) Act, people invested in qualified retirement plans and IRAs were required to begin taking required minimum distributions (RMDs) from those plans after they turned 70 ½.

Prior to the enactment of the SECURE (Setting Every Community Up for Retirement Enhancement) Act, people invested in qualified retirement plans and IRAs were required to begin taking required minimum distributions (RMDs) from those plans after they turned 70 ½.

Under the SECURE Act, the age for beginning RMDs is now 72 for all those who turn 70 ½ after December 31, 2019. Calculating the amount of those RMDs will also change due to an update to life expectancy tables proposed by the IRS, which are scheduled to take effect in 2021.

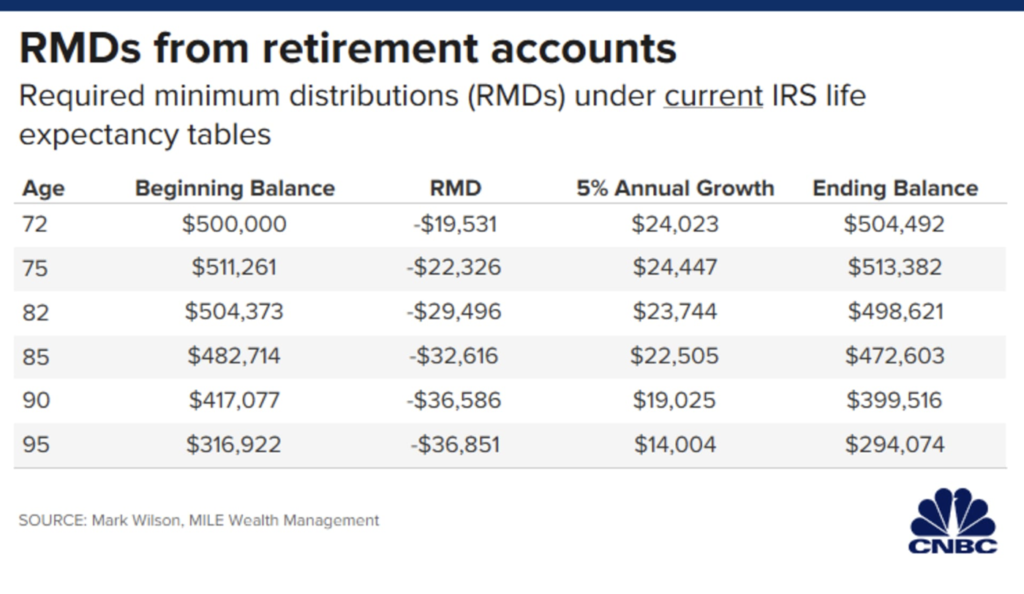

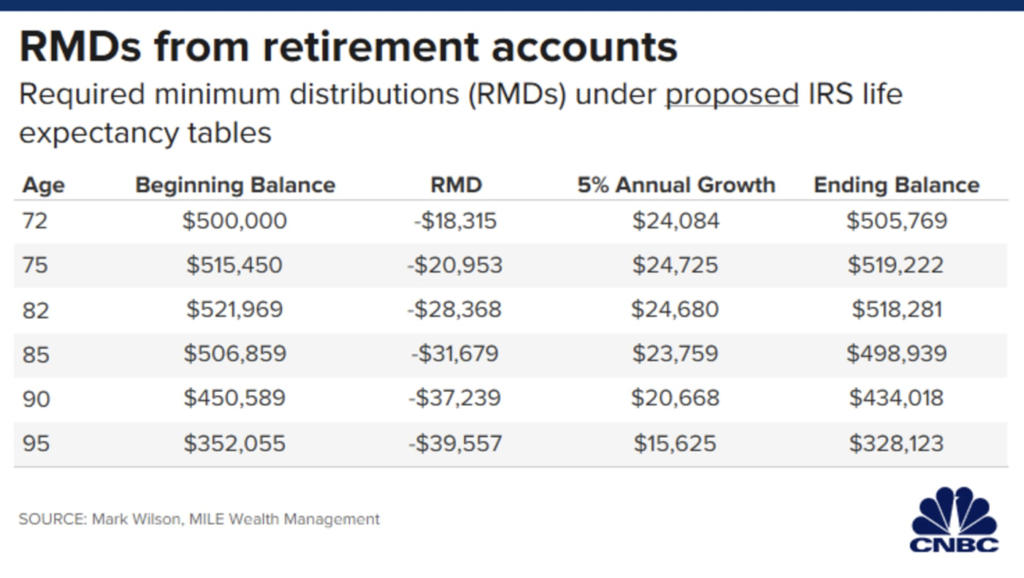

A recent CNBC article provided comparison charts to illustrate how RMD amounts and account balances would differ if the IRS proposed changes are implemented:

Since the IRS estimates that just 20% of those with qualified retirement plans take only the minimum required distribution — meaning that a vast majority of retirees take more than the minimum — these life expectancy table modifications are unlikely to have a dramatic effect.

However, when considered in conjunction with the increase to age 72 for requiring RMDs, these changes could mean a reduction in income taxes since the payout period increases, thereby decreasing the distribution amount. The lowering of a taxpayer’s modified adjusted gross income (MAGI) may help avoid the net investment income tax of 3.8% as well as taxes on Social Security benefits and Medicare premium surcharges.

The ERISA attorneys at Hall Benefits Law help our clients manage legislative and regulatory changes to all variety of benefit plans, including handling changes to plan documents and advising on how to implement corresponding procedures. To learn more or to get help making changes to your plans today, call 678-439-6236.