On July 9, 2021, the Pension Benefit Guaranty Corporation (PBGC) issued an interim final rule (IFR) on the process for eligible distressed multiemployer pension plans to calculate and apply for Special Financial Assistance (SFA) awards under the American Rescue Plan Act of 2021 (ARPA). Following is a summary of the key components of the IFR:

On July 9, 2021, the Pension Benefit Guaranty Corporation (PBGC) issued an interim final rule (IFR) on the process for eligible distressed multiemployer pension plans to calculate and apply for Special Financial Assistance (SFA) awards under the American Rescue Plan Act of 2021 (ARPA). Following is a summary of the key components of the IFR:

SFA Award Calculation

Plan sponsors that qualify for PBGC assistance may apply for a one-time lump sum payment to cover all benefits due through the 2051 plan year. The IFR establishes a more specific calculation in which the amount of SFA an eligible plan may receive equals the difference between the plan’s current and estimated future benefit obligations and the plan’s resources, including current assets, anticipated future contributions, and expected withdrawal liabilities. The calculation must be from the last day of the calendar quarter before the plan files for SFA through the end of the 2051 plan year.

SFA Application Timing and Payment

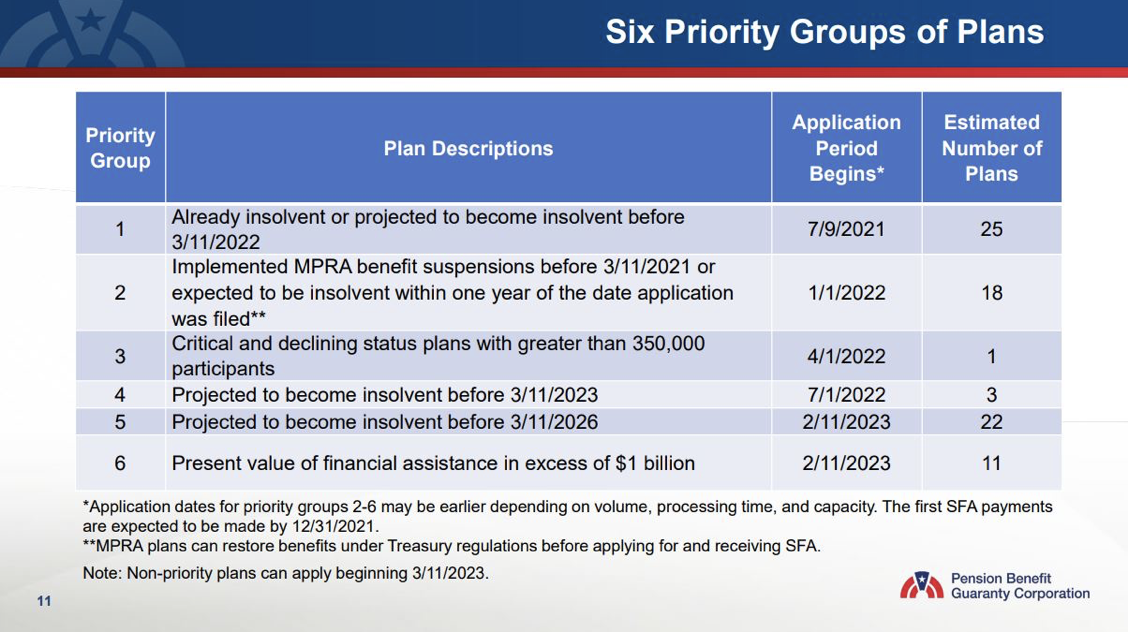

The IFR establishes six priority categories based on certain factors, including a distressed plan’s current funding status and insolvency date projection:

Under ARPA, the PBGC has 120 days in which to review SFA applications. Once an application is approved, a lump sum award will typically be paid within 60 to 90 days.

Withdrawal Liability

An earlier version of ARPA included a provision that would have disregarded SFA awards when it came to calculating withdrawal liability. However, that provision was subsequently struck from the final legislation. Instead, ARPA defers to the PBGC to address the treatment of SFA awards for withdrawal liability purposes.

Under the IFR, SFA awards are included in calculating a plan’s assets for withdrawal liability purposes. However, a plan that receives an SFA award is required to use the PBGC’s mass withdrawal interest rate assumptions when calculating withdrawal liability until the later of either (1) 10 years from the end of the plan year in which the SFA award is received, or (2) the last day of the plan year in which the plan no longer holds assets (or asset earnings) from the SFA award.

In addition, the IFR limits settling withdrawal liability disputes that exceed $50 million without PBGC approval.

Investment Restrictions

The IFR states that SFA awards must be kept separate from other plan assets and may only be invested in investment-grade fixed income securities. In addition, plans receiving SFA awards must allocate plan assets – including SFA award assets – in fixed income securities sufficient to cover one year of benefit payments and administrative costs.

HBL has experience in all areas of benefits and employment law, offering a comprehensive solution to all your business benefits and HR/employment needs. We help ensure you are in compliance with the complex requirements of ERISA and the IRS code, as well as those laws that impact you and your employees. Together, we reduce your exposure to potential legal or financial penalties. Learn more by calling 470-571-1007.