The Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE Act) added new lifetime income disclosure requirements to benefit statement rules under ERISA. The law now requires that a participant’s total accrued benefit be expressed as a lifetime income stream in the form of a single life annuity. If the participant has a same-age spouse, the total accrued benefit must be expressed as a qualified joint and survivor annuity. These lifetime income stream disclosures must be provided in one benefit statement during each 12-month plan period.

On September 18, 2020, the Department of Labor (DOL) published an Interim Final Rule (IFR) to the Federal Register to implement the lifetime income disclosure requirements pursuant to the SECURE Act. Once the lifetime income disclosure requirement becomes fully effective on September 18, 2021, defined contribution plan benefit statements must include lifetime income illustrations expressed in two forms: as a single life annuity (SLA) and a qualified joint and survivor annuity (QJSA).

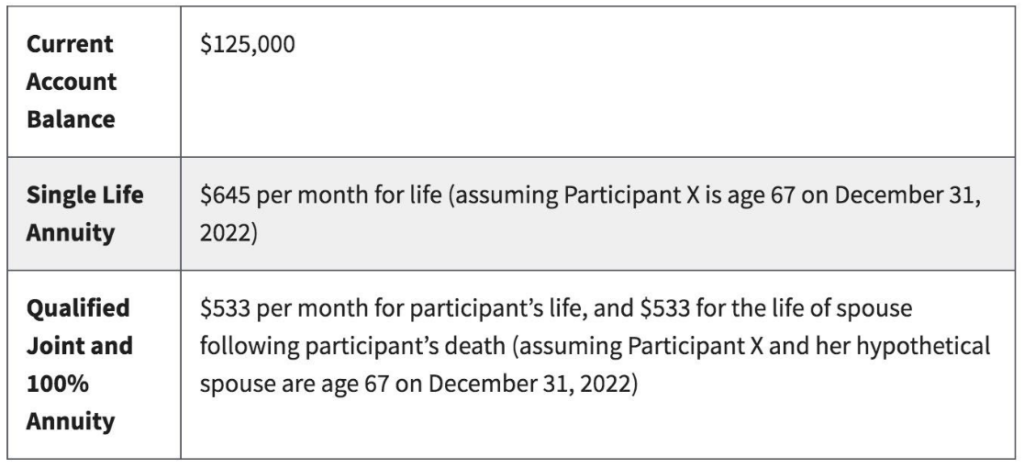

A lifetime income illustration is designed to help participants better understand how they are progressing toward their retirement savings goals. In preparing a lifetime income illustration, plan administrators must assume and consider the following when calculating a monthly payment illustration:

The Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE Act) added new lifetime income disclosure requirements to benefit statement rules under ERISA. The law now requires that a participant’s total accrued benefit be expressed as a lifetime income stream in the form of a single life annuity. If the participant has a same-age spouse, the total accrued benefit must be expressed as a qualified joint and survivor annuity. These lifetime income stream disclosures must be provided in one benefit statement during each 12-month plan period.

On September 18, 2020, the Department of Labor (DOL) published an Interim Final Rule (IFR) to the Federal Register to implement the lifetime income disclosure requirements pursuant to the SECURE Act. Once the lifetime income disclosure requirement becomes fully effective on September 18, 2021, defined contribution plan benefit statements must include lifetime income illustrations expressed in two forms: as a single life annuity (SLA) and a qualified joint and survivor annuity (QJSA).

A lifetime income illustration is designed to help participants better understand how they are progressing toward their retirement savings goals. In preparing a lifetime income illustration, plan administrators must assume and consider the following when calculating a monthly payment illustration:

- The date when annuity payments will begin;

- The age of the participant once annuity payments begin;

- The SLA benefit with no survivor benefit;

- The QJSA benefit assuming a spouse of the same age, regardless of the participant’s marital status or the actual age of any spouse;

- The QJSA survivor benefit using a Qualified Joint and 100% Survivor Annuity;

- The assumed interest rate using the 10-year constant maturity Treasury rate (10-year CMT) as of the first business day of the last month of the statement period; and

- The assumed life expectancy using the gender neutral mortality table in section 417(e)(3)(B) of the Internal Revenue Code.

The IFR also includes a disclaimer that the periodic payment amounts in the illustration are not guaranteed and are being used only for illustration purposes. In addition, certain explanations must be included with the illustration such as an explanation of an SLA and a QJSA.

The DOL has also furnished model disclosure language that plan administrators can integrate into or appended to their existing benefits statements. If this model language is used, the IFR releases the plan administrator from liability solely based on the provision of lifetime income stream equivalents as outlined in the Final Rule.

The IFR also addresses a number of additional aspects of the disclosure, including special rules for plans with annuity distribution options.

The experienced, responsive team of ERISA attorneys at Hall Benefits Law helps plan administrators understand what regulations and rulings are relevant to them and how best to apply these rulings in practice. Learn more by calling 678-439-6236.

The IFR also includes a disclaimer that the periodic payment amounts in the illustration are not guaranteed and are being used only for illustration purposes. In addition, certain explanations must be included with the illustration such as an explanation of an SLA and a QJSA.

The DOL has also furnished model disclosure language that plan administrators can integrate into or appended to their existing benefits statements. If this model language is used, the IFR releases the plan administrator from liability solely based on the provision of lifetime income stream equivalents as outlined in the Final Rule.

The IFR also addresses a number of additional aspects of the disclosure, including special rules for plans with annuity distribution options.

The experienced, responsive team of ERISA attorneys at Hall Benefits Law helps plan administrators understand what regulations and rulings are relevant to them and how best to apply these rulings in practice. Learn more by calling 678-439-6236.